Silicon‑level IP control reshapes codec and chipset monetization economics.

Key Takeaways

- Modern SoC designs rely on licensed IP blocks, with less than 10% newly written code.

- Value has shifted toward SoC design intellectual property licensing and integration.

- Codec hardware acceleration follows a per‑unit royalty model, from a few cents to $1.20 per chip.

- ARM architectural license models generate hundreds of millions in quarterly royalties, proving the strength of the semiconductor IP licensing model.

- Foundries use process‑specific IP and design kits to create lock‑in, extending control across the semiconductor ecosystem and chip manufacturing ecosystem.

Introduction

The battleground for value in semiconductors has shifted from software into silicon. Hardware acceleration for video codecs and the semiconductor IP licensing model now dominate, with system on chip (SoC) IP monetization turning codec economics into a chip‑level business built on royalties and control points.

In this study, we explore SoC licensing models and royalty economics, embedded codec IP and hardware acceleration, foundry leverage and IP lock‑in, and hardware acceleration as both technical and economic control.

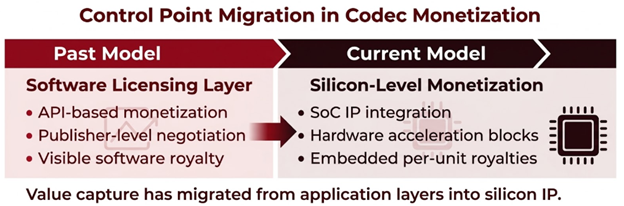

The Control Point Migration

Modern SoC designs are increasingly driven by intellectual property management. IP assembly consumes most project resources before physical design begins. Chip designers must define requirements, select vendors, customize products, set parameters, and integrate dozens of IP blocks with hundreds of instances into a working system.

This complexity shows how hardware acceleration for video codecs and embedded codec IP have become central levers for SoC IP monetization. Beyond technical performance, these elements create new semiconductor royalty revenue streams, enforce foundry IP lock‑in, and establish economic control points that were once managed through software.

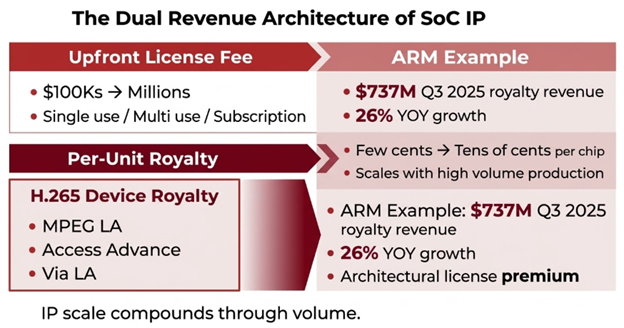

SoC Licensing Models and Royalty Economics

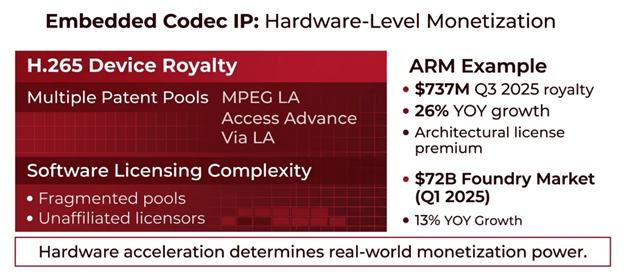

The SoC architecture licensing model operates on upfront fees plus per‑unit royalties. Vendors charge hundreds of thousands to millions for licenses, then collect ongoing royalties. ARM’s model illustrates this clearly. Its chipset royalty revenue model generated $737 million in Q3 2025, a 26% year‑over‑year increase.

The legal disputes surrounding these models reveal their economic significance. The recent ARM Qualcomm litigation centered on whether architectural licenses transfer through acquisitions. ARM claimed the licensing fee discrepancy resulted in an estimated annual revenue loss of $50 million, highlighting the high stakes involved in IP transfer terms and architectural licensing boundaries.

Embedded Codec IP and Hardware Acceleration

Video codec intellectual property is a prime example of hardware‑based monetization. The codec licensing ecosystem has grown complex, where hardware acceleration support determines adoption and revenue. H.265/HEVC, managed by MPEG LA, Access Advance, and Via LA, requires licensing fees, with device royalties reaching up to $1.20 per unit for 4K televisions.

This licensing model produced a split outcome. By 2025, all smart TVs and OTT devices supported HEVC, proving commercial success in hardware platforms where codec IP is embedded into SoC designs. Device makers absorbed per‑unit costs, spread across millions of units, justified by the competitive need for 4K HDR delivery.

In contrast, software publishers faced adoption barriers. Licensing uncertainty and fragmented patent pools created risks. Negotiating with three pools plus unaffiliated licensors like Nokia added legal and financial complexity, which many smaller publishers avoided. When codec IP is embedded in hardware through SoC integration, licensing complexity is absorbed at the chip stage, insulating developers and content platforms from direct patent exposure.

The rise of AV1, backed by the Alliance for Open Media, offered a royalty‑free alternative to HEVC. Yet adoption depends on hardware acceleration. Without dedicated silicon, AV1 software decode runs 5–10 times slower than VP9, making it commercially impractical for high‑volume applications. This shows how hardware acceleration and silicon‑level IP monetization continue to define codec economics and market control.

Foundry Leverage and IP Lock‑In

Foundries like TSMC and Samsung play a bigger role than manufacturing. They build design optimization kits (DOKs) with EDA partners to help SoC designers hit performance and efficiency targets. These kits create process‑specific lock‑in, since IP optimized for one foundry often needs major rework to move to another.

The global semiconductor foundry market reached $72 billion in Q1 2025, with 13% year‑over‑year growth driven by AI chip demand. This scale gives foundries strong leverage in the IP licensing ecosystem. When codec or connectivity IP is tied to foundry processes, technical dependency becomes economic control.

Foundries also provide embedded IP libraries such as logic, memory, and interface IP. Designers gain confidence and PPA optimization but lose portability. Codec IP inside these blocks carries its own licensing terms, creating layered monetization where both IP vendors and foundries capture value.

Hardware Acceleration as Technical and Economic Control

Hardware acceleration moves codec deployment from software into silicon. When H.265 or AV1 decode is built into SoC hardware blocks, licensing changes. Negotiations happen at chip design time. Royalties embed in the chip bill of materials. Technical dependencies persist across product generations.

The maturity gap shows this control. H.265 hardware acceleration is widespread across Android 5.0+, macOS High Sierra+, and modern Windows devices. This comes from years of IP development and SoC integration. AV1 hardware support is newer, limited to Android 10+, select decoder chips, and recent smart TVs. This creates market fragmentation that influences codec adoption.

Performance reinforces hardware control. H.265 hardware acceleration uses far less CPU than AV1, which is critical for live streaming. Without hardware support, AV1 encoding is 5–10 times slower than VP9. This makes AV1 impractical at scale. Adoption requires chip‑level integration, creating a coordination loop. Content providers wait for hardware. Hardware makers wait for content. IP vendors capture value through SoC licensing.

Final Strategic Takeaways

The semiconductor royalty business model is shifting toward embedded IP. Codec and connectivity control now reside in silicon, favoring companies with strong IP portfolios and advanced SoC design capabilities. Hardware acceleration for video codecs determines success. HEVC codec licensing costs were absorbed through hardware integration, while software‑only models struggled. As standards fragment, chipset intellectual property licensing and hardware codec integration will define winners in the codec patent ecosystem.

Future growth depends on system on chip (SoC) IP monetization and silicon‑level IP control. Companies that master SoC architecture licensing models, avoid foundry IP lock‑in, and expand into semiconductor IP revenue models will capture value in the evolving semiconductor ecosystem.

Recommendations for Stakeholders

- Chip Designers

- Prioritize ARM architectural license models and clarify transfer terms.

- Avoid lock‑in by selecting multi‑foundry verified IP blocks.

- Content Platforms

- Factor in HEVC vs AV1 hardware acceleration support when planning streaming strategies.

- Align with chipset vendors on codec timelines.

- IP Vendors

- Develop foundry‑agnostic IP to reduce risk.

- Expand into silicon architecture licensing and bundled services.

- Foundries

- Bundle chip design monetization services with fabrication.

- Capture value through process‑specific IP integration.

- Regulators and Policy Makers

- Monitor semiconductor royalty business models to balance innovation with fair competition.

- Ensure transparency in video codec IP licensing economics.