SEP Licensing Beyond Smartphones to IoT Patent Licensing and Automotive Connectivity

Key Takeaways

- SEP value is shifting beyond smartphones into automotive, industrial IoT, and consumer devices.

- Market fragmentation is replacing handset‑era concentration, making negotiations more complex.

- Licensing models are diversifying: per‑device, flat per‑vehicle, component‑level, and pass‑

- Multi‑jurisdictional enforcement adds complexity, with courts in Germany, UK, China, US, and India shaping outcomes.

- Standards bodies face mounting pressure as FRAND governance struggles to scale across diverse industries.

Introduction

The era of smartphone patent wars is fading. Disputes such as Apple versus Samsung or Qualcomm versus major handset makers defined a decade of SEP enforcement and shaped FRAND case law. The importance of standard essential patents (SEP) licensing remains, but their value is now shifting. Connectivity powered by connected device patents is no longer limited to smartphones. It is built into vehicles, factory equipment, medical devices, home appliances, and industrial systems. This change is transforming SEP monetization economics. The handset model was never designed to handle such diverse markets. Global IoT adoption is rising quickly. Research shows connected IoT devices surpassed 16 billion in 2023 and are expected to exceed 29 billion by 2027. Growth is strong across automotive, industrial, and consumer markets.

Cellular IoT licensing markets are expanding, driven by telematics and smart industry applications. Despite this surge, licensing revenues outside smartphones have not grown at the same pace. The reason lies in structural differences between markets. Fragmented supply chains, lower margins, and longer product lifecycles make smartphone royalty models difficult to apply to IoT and automotive ecosystems. This study examines the evolution of SEP licensing across smartphones, IoT, and automotive markets, focusing on market structures, pricing models, enforcement, industry challenges, and governance pressures.

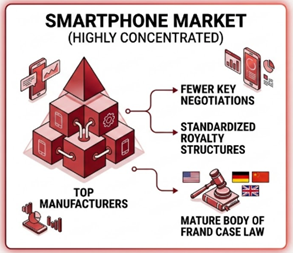

The Concentration Advantage That Powered Smartphones

Smartphone SEP licensing grew rapidly because the market was highly concentrated. A small group of manufacturers produced most of the world’s devices, making negotiations manageable. Royalty structures, often based on wholesale price percentages or per‑unit fees, became standardized over time. Years of litigation in the United States, Germany, China, and the United Kingdom created a mature body of FRAND case law.

This model does not translate well to new categories. Connected vehicles, for example, rely on complex supply chains with telematics units, communication modules, infotainment systems, and V2X features sourced from multiple vendors. Smart home devices are often built by smaller companies with thin margins. Industrial IoT deployments may involve tens of thousands of devices in a single facility, with lifecycles far longer than consumer electronics.

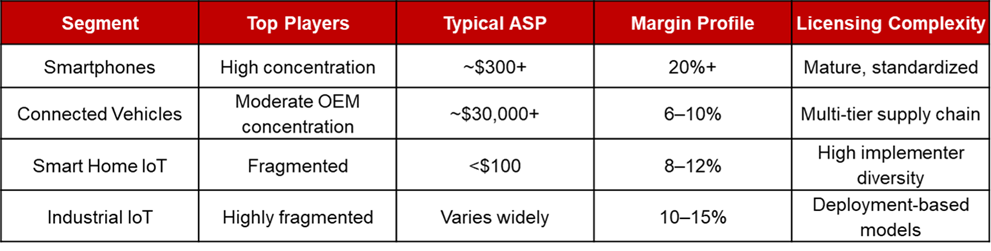

Market Structure Comparison

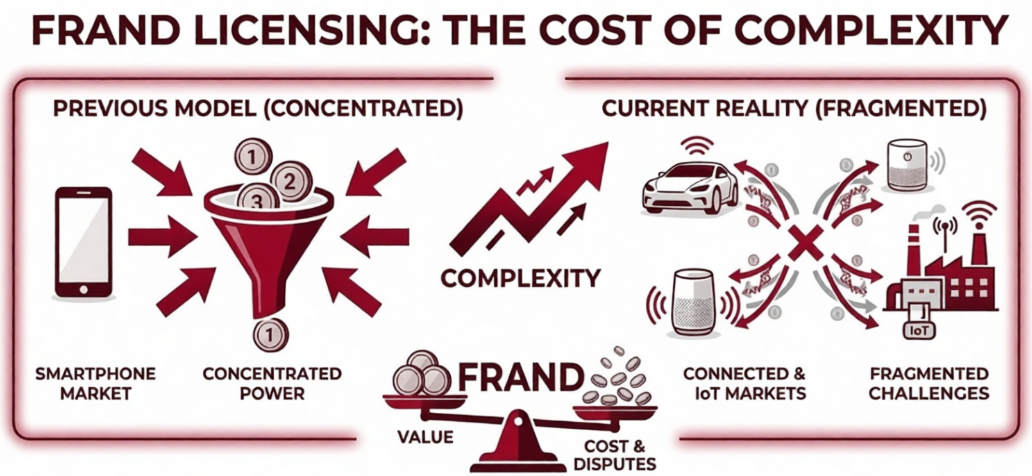

The concentration advantage in cross-industry SEP licensing no longer exists in IoT and automotive markets. In smartphones, a few large manufacturers dominated global shipments, making negotiations more efficient and royalty structures more predictable. IoT and automotive ecosystems are far more fragmented. Vehicles integrate multiple modules from different suppliers, while smart home devices are often produced by smaller companies with limited margins. Industrial IoT deployments can involve tens of thousands of devices in a single facility, with lifecycles much longer than consumer electronics. This fragmented market structure makes licensing negotiations more complex and reduces the efficiency of traditional global portfolio models. SEP holders and implementers must now adapt strategies to reflect diverse industry economics rather than relying on the smartphone template.

Licensing Challenges

SEP licensing is no longer confined to smartphones. As connectivity expands into vehicles, factories, and consumer devices, new challenges are reshaping how royalties are negotiated and enforced. Licensing challenges in SEP monetization can be grouped into three key areas:

- The End-Device Licensing Debate: A major issue in SEP licensing is deciding where in the value chain it should take place. SEP holders push for licensing at the finished product level, while automotive manufacturers argue it should be at the component level since they use modules from suppliers. Courts, including Sisvel v. Haier, have clarified FRAND negotiation rules, but disputes continue across Europe and Asia. This ongoing debate has slowed monetization, leaving many connected vehicles without full licensing coverage.

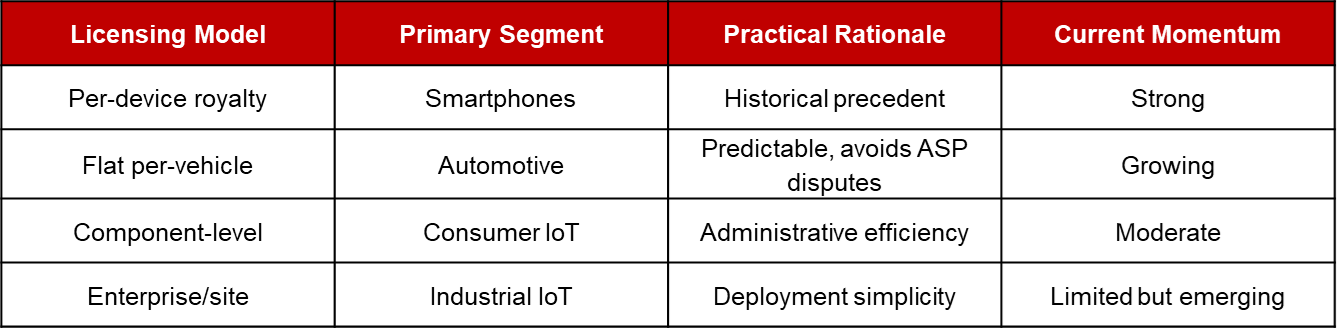

- SEP royalty model are evolving: Smartphones still rely on per‑device royalties. This model works well for handsets but is less suited to other industries. Automotive licensing is shifting to fixed per‑vehicle pricing. Platforms like Avanci set clear rates, such as $20 for a 4G vehicle and $32 for a 5G vehicle. This approach gives predictability and avoids percentage‑based calculations that OEMs reject. Industrial IoT faces different challenges. Factories may run thousands of devices for more than a decade. Here, component‑level licensing and indemnification by chipset suppliers are common. Semiconductor vendors include licensing costs in module pricing, giving enterprise buyers legal certainty. Consumer IoT often uses chipset-level patent licensing models. This lowers royalty income per unit but reduces transaction friction and enforcement complexity in fragmented markets.

- Comparative Licensing Approaches : Licensing models vary across industries and reflect the economics of each segment. In smartphones, per‑device royalties remain the standard approach. Automotive licensing has shifted toward flat per‑vehicle pricing, offering predictability and avoiding disputes over percentage‑based calculations. Industrial IoT often relies on component‑level or enterprise/site licensing, where costs are absorbed by chipset suppliers and spread across large deployments. Consumer IoT typically uses pass‑through models at the chipset level, which simplify compliance but reduce royalty yield per unit. Together, these approaches highlight how SEP monetization must adapt to the unique dynamics of smartphones, automotive, consumer IoT, and industrial IoT markets.

Industry Battlegrounds

SEP monetization faces its toughest challenges in industries where connectivity is both high‑value and deeply fragmented. Automotive, industrial IoT, and the role of non‑practicing entities (NPEs) represent the most contested battlegrounds. These sectors highlight how supply‑chain complexity, risk sensitivity, and market fragmentation reshape enforcement and licensing strategies:

- The Automotive Bottleneck: Automotive SEP licensing is the most valuable battleground. Vehicle connectivity now includes telematics, infotainment, V2X communication, and over‑the‑air updates. Mapping patents to these subsystems requires detailed technical analysis, often only done during litigation. Licensing pools and structured programs help reduce friction. However, supply‑chain responsibility remains disputed. Tier‑1 suppliers resist broad obligations, while OEMs avoid direct negotiations that could lead to royalty stacking. As a result, revenue realization is slower than in the smartphone era.

- Industrial IoT and Risk Sensitivity: Industrial buyers face unique risks. A patent injunction on a connected production line could stop operations worth millions each day. To avoid this, companies prefer “patent‑safe” components with indemnification. This shifts monetization upstream to semiconductor and module providers. Larger SEP holders with broad portfolios benefit, while smaller ones struggle to enforce rights in fragmented deployments.

- NPEs and Market Fragmentation: Non‑practicing entities once thrived in concentrated handset markets. Today, IoT ecosystems are highly distributed, making enforcement costly and inefficient. Many NPEs now target automotive OEMs or partner with operating companies to strengthen leverage. Fragmentation is reshaping both enforcement economics and connectivity strategies.

Governance and Enforcement Pressures

SEP monetization is shaped not only by licensing models but also by the legal frameworks and governance structures that define how disputes are resolved. Enforcement strategies and systemic pressures together illustrate the complexity of managing global portfolios across fragmented industries. Ultimately, the balance between legal enforcement and standards governance will determine whether SEP licensing adapts smoothly to connected technologies or remains constrained by smartphone‑era assumptions.

- Enforcement Strategies: Global SEP enforcement strategies now requires coordinated action across different legal systems. Germany is favored for its strong injunction framework, while the United Kingdom has become a key forum for setting global FRAND rates. China’s courts are increasingly shaping licensing terms, and the United States focuses more on damages than injunctions after the eBay ruling. India takes a more implementer‑friendly approach, often using escrow‑based interim solutions. These differences create strategic opportunities but also make global portfolio negotiations more complex.

- Systemic Pressures: Standards bodies like ETSI and IEEE were not designed to handle cross‑industry royalty conflicts. FRAND commitments remain contractual, and defining “fair and reasonable” compensation continues to spark debate. As automotive, IoT, and cloud players join standard development, governance becomes more complex. The challenge is not whether SEPs deserve compensation, but how that compensation should scale when connectivity is embedded in everything from tractors to thermostats.

Wrapping Up

The shift from handset‑centric SEP monetization model to connected‑everything licensing is structural, not temporary. SEP holders must tailor pricing strategies to each industry. Implementers need in‑house licensing expertise. Component suppliers are gaining bargaining power as intermediaries. The next decade will decide whether SEP economics adapt to fragmented ecosystems or remain tied to outdated smartphone models.

Recommendations for Stakeholders

- SEP Holders: Segment pricing strategies by industry instead of relying on smartphone benchmarks.

- Implementers (OEMs & IoT Manufacturers): Build in‑house SEP expertise and negotiate supply‑chain responsibilities early.

- Component & Semiconductor Suppliers: Offer indemnified, patent‑cleared modules to strengthen bargaining leverage.

- Policy Makers & Standards Bodies: Enhance governance frameworks to manage cross‑industry royalty allocation disputes.

- Investors & Market Analysts: Monitor automotive and industrial IoT licensing trends as leading indicators of SEP monetization growth.