Rethinking chocolate formulation amid cocoa supply, cost, and climate pressures

Key Takeaways

- Structural Cocoa Risk: Cocoa supply challenges are no longer temporary. Climate pressure, disease, and tighter regulations are turning cocoa volatility into a long-term business risk for chocolate manufacturers.

- Dual Replacement Strategy: Cocoa solids and cocoa butter play very different roles in chocolate. Addressing them separately allows formulators to make smarter, lower-risk substitution decisions.

- Practical Near-Term Options: Carob offers a realistic starting point for reducing cocoa solids without compromising taste. Regional alternatives can further strengthen supply resilience over time.

- Flexible Fat Systems: There is no single solution for replacing cocoa butter. Using a mix of fats such as sal, kokum, and wild mango allows products to perform better across different climates and markets.

- Early Action Advantage: Turning cocoa alternatives into real products requires early supplier alignment and pilot testing. Companies that move early can reduce formulation risk and stay ahead of cost volatility.

Introduction

The global cocoa industry is facing very high pressure, with climate volatility, diseases, and aging plantations in West Africa. This is driving the significant price increases in the chocolate sector which has seen in decades. For R&D teams, this has turned cocoa dependency into a formulation and business-continuity challenge. Thus, ingredient scouting is becoming increasingly important for companies exploring potential substitutes that can replicate cocoa’s complex functionality, both in terms of cocoa solids (flavor, color, polyphenol chemistry) and cocoa butter (fat structure, melt behavior), while also remaining commercially viable.

The solution space can be broadly divided into two distinct categories: cocoa solid alternatives and cocoa butter alternatives. On the cocoa solids side, carob is gaining traction as a credible short-term option, as it can deliver cocoa-like flavor and color profiles while offering versatility across applications. In parallel, a new generation of cocoa butter alternatives is emerging, ranging from structurally similar seed fats such as sal, wild mango, and kokum to advanced fat-structuring systems like oleogels. Together, these approaches create opportunities to develop more resilient hybrid formulations.

Rather than relying on a single substitute, the most effective path forward lies in combining ingredients from both categories. By diversifying formulations and supporting them with early supplier alignment and pilot-scale testing, brands can better stabilize product quality, manage costs, and accelerate more sustainable chocolate innovation.

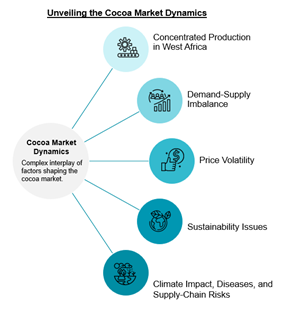

Current Cocoa Market & Challenges

The global cocoa market is under sustained pressure from supply concentration, demand growth, and evolving regulatory expectations.

- Concentrated Production in West Africa

Global cocoa production remains highly concentrated, with Côte d’Ivoire and Ghana together accounting for almost half of the world’s cocoa output (~46%), making the supply chain especially vulnerable to regional disturbances. In the 2023/24 cocoa season, Côte d’Ivoire produced about 2.38 million tons, or roughly 42% of global production, while Ghana contributed around 11-20% of global supply, depending on sources and annual variations. Both countries continue to face climate-related risks such as heat stress, erratic rainfall, and soil degradation, which can suppress yields and increase supply uncertainty.

- Demand-Supply Imbalance

Consumer demand for chocolate will continue to increase in both the established as well as emerging markets. Cocoa production has struggled to keep pace. In the 2023/24 season, global cocoa production was around 4.4 million tonnes, placing pressure on supply given rising consumption and historically low stocks in major exchange warehouses. The increasing gap has created significant structural deficits that cannot be addressed at the conventional cocoa supply footprint.

- Price Volatility

Volatile market conditions and the accelerated changes in cocoa pricing are putting immense pressure on manufacturers. The economic uncertainty caused by fluctuating cocoa prices is compelling companies to reconsider long-term sourcing relationships and launch significant formulation analyses.

- Sustainability Issues

Ongoing concerns about deforestation, farmer welfare, and a lack of transparency in supply chains have brought cocoa into sharper regulatory focus. The EU Regulation on Deforestation-Free Products (EUDR), formally adopted in June 2023, mandates that cocoa and other forest-risk commodities placed on the EU market must be deforestation-free and traceable to origin, based on land use since 31 December 2020. Compliance deadlines are phased, with most companies needing to meet the requirements by 30 December 2025 and smaller enterprises by 30 June 2026.

- Climate Impact, Diseases, and Supply-Chain Risks

Cocoa trees are exceptionally sensitive to environmental stress. Diseases like black pod and swollen shoot virus, combined with rising temperatures and unpredictable rainfall, are reducing production reliability and reinforcing the need for alternative ingredient pathways.

Cocoa Solid Alternatives: Flavor, Color, and Polyphenol Replacements

Carob consistently emerges as the strongest near-term cocoa solid alternative. Jackfruit seeds show moderate formulation potential, while red oak acorns remain more exploratory due to scale and consistency constraints.

Carob consistently outperforms other substitutes because it offers not only a closer sensory resemblance to cocoa but also a more balanced functional profile. Its natural sweetness, caramel flavor, and dark hue all provide sensory advantages to formulators, while its polyphenolic framework helps develop cocoa aroma without risking bitter off notes. Research shows that carob can replace a meaningful proportion of cocoa solids in either milk or dark chocolate formulation without notable differences in taste, texture, or melt behavior. This positions carob as an ingredient that reduces formulation risk while offering immediate commercial feasibility. Carob strikes the ideal balance of sensory appeal, functional performance, and practical availability, making it the strongest starting point for reducing cocoa solid dependence without compromising product quality.

Jackfruit seeds present a compelling case for circular economy approaches to cocoa replacement. Typically discarded as waste, these seeds can be fermented, roasted, and converted into flour that imparts a distinct chocolate aroma. Brazilian research has demonstrated that roasted jackfruit seed flour can replace 50% to 75% of cocoa powder in cappuccino and chocolate formulations without compromising sensory acceptance. The chocolate-like aroma develops through Maillard reactions during roasting. As jackfruit seeds are rich in nutrients and naturally develop chocolaty notes when processed, they represent a scalable solution for manufacturers seeking to diversify away from conventional cocoa solids.

When roasted, red oak acorns develop a flavor and aroma profile remarkably similar to cocoa powder. The roasting process enhances sensory characteristics and increases polyphenolic content and antioxidant properties, which are critical functional attributes in cocoa replacement. Studies have demonstrated that roasted red oak acorn powder can partially substitute cocoa powder in chocolate formulations while maintaining acceptable sensory properties. This alternative is particularly attractive from a sustainability perspective, as acorns are an abundant and underutilized resource in many temperate regions.

While carob remains the most viable near-term cocoa solid substitute, long-term resilience will depend on selectively integrating region-specific alternatives.

Red oak acorns offer manufacturers in North America and Europe a pathway to reduce reliance on tropical cocoa by leveraging locally abundant, renewable resources with acceptable sensory performance. In parallel, jackfruit seeds present a scalable circular-economy opportunity in South and Southeast Asia, enabling companies to convert agricultural by-products into viable cocoa alternatives.

Cocoa Butter Alternatives: Fat Structure and Melt Profile Replacements

Cocoa butter replacement presents a distinct formulation challenge focused on replicating the unique crystalline structure, snap, gloss, and melt-in-mouth characteristics that define premium chocolate.

Sal fat features a triglyceride composition led by stearic and oleic acids that closely mirrors cocoa butter’s crystalline behavior. This similarity translates directly into the characteristic snap, gloss, and melt-at-body-temperature properties that consumers expect. From a formulation perspective, sal fat demonstrates excellent compatibility with cocoa butter in blended systems, allowing for gradual substitution without dramatic reformulation. Its melting point and polymorphic behavior align well with chocolate processing requirements, including tempering protocols and bloom resistance. Sal fat also offers supply chain diversification benefits, as sal trees are cultivated across India and Southeast Asia.

For chocolate formulations intended for distribution in warm climates, kokum butter provides clear benefits. Its high stearic acid content often provides more than 50% firmness and thermal stability. This thereby solves a major problem for producers catering to tropical and subtropical markets where traditional chocolate suffers from bloom and softening. Blending kokum with lower-melting fats offers significant opportunities for product differentiation, even though this elevated melting point necessitates careful formulation to maintain desired mouthfeel. Additionally, the natural oxidation resistance of kokum prolongs the shelf life of products.

The triglyceride profile of wild mango kernel fat is comparable to that of cocoa butter, with balanced amounts of unsaturated and saturated fatty acids that support favorable melting and crystallization patterns. The remarkable thermal stability of wild mango kernel fat during processing and storage, which lowers the possibility of fat bloom and increases product shelf life, is what sets it apart. Manufacturers that operate in areas with uneven cold chain infrastructure will especially benefit from this stability. Additionally, the fat from wild mango kernels shows good compatibility with other specialty fats, allowing formulators to create hybrid fat systems.

Rather than viewing cocoa butter alternatives as one-to-one replacements, leading manufacturers should adopt a portfolio fat strategy aligned to market conditions and distribution realities. Sal fat offers the fastest route to cost and supply diversification with minimal operational disruption, making it ideal for near-term reformulation. Kokum butter enables the design of heat-resilient chocolates tailored to tropical markets, where traditional cocoa butter performance is structurally constrained. Wild mango kernel fat addresses logistical risk by improving product stability in regions with unreliable cold chains.

Conclusion: Rethinking Cocoa Dependency

Together, these fats enable companies to move beyond a single cocoa butter dependency and build regionally optimized, risk-adjusted chocolate fat systems that balance sensory quality, supply resilience, and commercial scalability.

Early supplier collaboration, pilot-scale testing, and focused sensory mapping will be essential to validate feasibility across both ingredient categories. Companies that invest now in diversified cocoa alternative ecosystems strategically addressing both the solid and butter components will be better positioned to stabilize portfolios, manage cost volatility, and lead in sustainable chocolate innovation.

Recommendations for Stakeholders

- Chocolate Manufacturers: Adopt a dual-track reformulation strategy that separately addresses cocoa solids and cocoa butter functionality. Blended, region-specific ingredient systems will reduce risk without compromising sensory quality.

- R&D Teams: Move early into pilot-scale trials combining cocoa alternatives rather than testing single substitutes. Sensory mapping and process validation should guide scalable, low-risk reformulation decisions.

- Ingredient Suppliers: Position alternatives such as carob, sal, kokum, and wild mango as part of integrated solution portfolios. Providing application support and formulation data will accelerate customer adoption.

- Procurement Teams: Shift sourcing strategies from single-origin dependency toward diversified, regional supply networks. Early supplier alignment can help stabilize costs and ensure regulatory and supply continuity.

- Sustainability & Strategy Leaders: Embed cocoa alternatives into long-term sustainability and compliance planning. Diversified ingredient ecosystems will support EUDR readiness while strengthening supply-chain resilience.