The Battle Between Device Makers, Chip Vendors, and Platform Giants: Who Owns the Stack

The Stack Power Struggle: Device Makers Rebel, Arm Escalates, Platforms Dominate

Key Takeaways

- Semiconductors shift back to vertical integration, driven by AI, 5G, and semiconductor stack economics.

- Arm raises fees up to 300%, moving chip IP licensing from chip vendors to device makers, sparking an Arm licensing conflict.

- Apple, Google, Amazon design proprietary silicon; AI chip market hits $500B by 2026.

- Regulators intensify scrutiny with DOJ antitrust review lawsuit (2024) and EU Digital Markets Act fine (2025).

- A three‑way struggle emerges: device makers seek independence, vendors defend revenues, platforms tighten platform control.

Introduction

The semiconductor industry is entering a period of disruption. The global market is expected to reach US$975 billion in annual sales in 2026, driven by the AI boom. Growth is colliding with rising chip licensing fees, vertical integration, and regulatory battles over platform control. Vertical integration is reshaping silicon and software. The Arm licensing conflict is creating tension. Operating systems are tightening control. Regulation is changing market structure.

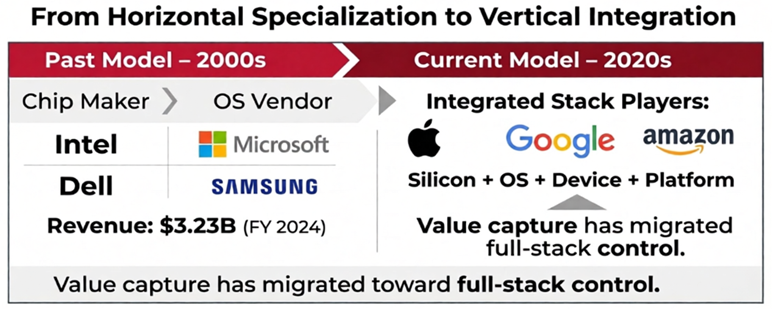

The Return of Vertical Integration

Arm licensing model shift diagram. The technology industry is shifting back to semiconductors vertical integration. For decades, horizontal specialization defined the market. Intel built chips, Microsoft supplied operating systems, and Dell assembled devices. That model is collapsing. Value now flows from technology to use cases. Cloud platforms and system integrators are moving upstream into silicon design to better monetize data and user experience. Apple shows the clearest example. Its M series processors have reshaped the laptop market. Five years after the M1 launch, Apple holds about 20 percent of processor share, rivaling AMD. Performance gains are steep. The M4 delivers 60 percent more speed than the M1. Apple’s goal is clear: control silicon to align with its software-hardware alignment and user priorities. Amazon follows a similar path. AWS Graviton chips cut energy use by 60 percent and improve price performance by 40 percent compared to x86. The aim is not to dominate chips but to reduce reliance on Intel and AMD while optimizing AI workload optimization and cloud economics. Google has taken the same route with Tensor processors. Built for Pixel devices, they focus on on-device AI and tight integration with Google’s software stack. Production has moved to TSMC’s 3nm process, giving Google more semiconductor supply chain control.

The Arm Dilemma and Licensing Warfare

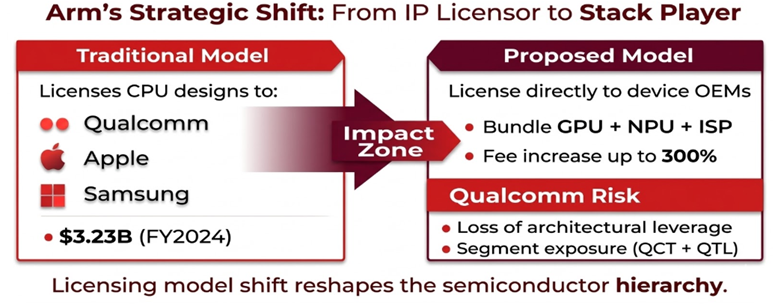

Arm Holdings sits at the center of the industry’s realignment. Its architecture powers billions of mobile devices worldwide. In January 2025, Reuters reported that Arm plans to raise chip licensing fees by up to 300 percent. The company is also considering designing complete chips, putting it in direct competition with customers such as Qualcomm, Apple, and Samsung. The issue goes beyond pricing. Court filings in Arm’s case against Qualcomm revealed plans to change its business model. Arm would stop licensing CPU designs to semiconductor vendors under traditional agreements. Instead, it would license directly to device makers. This shift would force manufacturers to adopt Arm’s GPU, neural processing unit, and image signal processor designs, limiting alternatives from AMD, Imagination Technologies, or in-house solutions.

Arm’s goal is to capture more of the value chain. Despite enabling the smartphone revolution and energy-efficient data center processors, Arm earned only $3.23 billion in fiscal 2024 revenue. By contrast, Apple’s hardware revenue was more than 90 times larger. For Qualcomm, the risk is severe. Its QCT division designs chips, while QTL collects royalties based on device sales. If Arm bypasses chip vendors and licenses directly to Samsung, Xiaomi, or other manufacturers, Qualcomm loses both its architectural foundation and its chip vendor differentiation. Three customers already account for more than 10 percent of Qualcomm’s revenue, making the threat existential. This Arm licensing conflict, tied to Arm patent portfolio, licensing model changes, and royalty and fee structure, represents a pivotal shift in industry economics.

Platform Control and Operating System Leverage

Operating system control is the strongest moat in the stack. Apple’s iOS ecosystem shows this power. In March 2024, the U.S. Department of Justice filed an DOJ antitrust review case, alleging Apple restricted app distribution and imposed anti-competitive rules. The case continues after Apple’s motion to dismiss was denied in June 2025. Europe has gone further. Under the EU Digital Markets Act, the EU fined Apple €500 million in April 2025 for blocking developers from promoting alternative payment options. The DMA requires gatekeepers like Apple, Google, and Meta to allow third-party app stores, enable interoperability standards, and avoid self-preferencing. Microsoft’s Windows on ARM highlights the challenge of platform control. Despite years of collaboration with Qualcomm, the platform struggles with app compatibility and performance parity with x86. This limits Microsoft’s ability to break Intel’s long-standing dominance.

Market Structure and Regulatory Headwinds

Concentration across the stack has triggered regulatory pushback. The FTC challenged Microsoft’s $69 billion Activision Blizzard deal as a vertical integration threat. Microsoft prevailed, but the case showed regulators are ready to scrutinize expansion even in adjacent markets. Deloitte projects the semiconductor market trends will near $1 trillion by 2026, with AI chip revenue forecast reaching $500 billion. Growth is uneven. AI data centers consume memory and storage at rates that create shortages for consumer electronics. Companies that control both chip design and platforms secure foundry capacity, leaving pure-play vendors at a disadvantage. Governments are responding with sovereignty initiatives. The U.S., EU, Japan, and Middle Eastern nations are funding domestic fabrication and packaging to reduce reliance on concentrated semiconductor supply chain. These policies favor vertically integrated firms with captive demand.

Final Strategic Takeaways

The technology stack is redistributing power. Companies that control silicon and software gain value by optimizing workloads, cutting costs, and protecting differentiation. Traditional chip vendors face pressure as licensing and general‑purpose models weaken. The Arm licensing conflict shows this tension, while customers explore proprietary silicon designs or open architectures like RISC‑V adoption. Regulatory action adds uncertainty, especially in Europe where platform control faces strict enforcement. Winners will be those that secure manufacturing capacity, maintain ecosystem lock‑in, and navigate antitrust scrutiny while sustaining integration. The future will be shaped by semiconductor innovation trends, vertical stack economics, chip design, platform leverage, and the evolution of the digital hardware ecosystem.

Recommendations for Stakeholders

- Chip Vendors

- Build differentiated IP in AI, security, and connectivity for cloud and automotive markets.

- Invest in RISC-V adoption and other open ISAs.

- Reduce reliance on Arm.

- Device Manufacturers

- Large firms should advance proprietary IP rights and custom chips.

- Smaller firms should secure multi-source supply options.

- Balance in-house silicon with vendor risks.

- Platform Operators

- Keep documentation clear to support semiconductors vertical integration.

- Prepare for platform operator regulation and scrutiny.

- Ensure interoperability standards and avoid bundling.

- Policymakers

- Structure subsidies to grow domestic capacity while protecting competition and consumer choice.

- Support next generation semiconductors and technology sovereignty.

- Avoid fragmentation.

- Regulators

- Monitor chip IP licensing, chip licensing fees, and platform control.

- Safeguard fair competition and balanced innovation incentives.

- Promote transparency.