Wi-Fi 8, 6G-Advanced, and the Next SEP Arms Race in Wireless Standards

How next-gen connectivity is redefining the global SEP battlefield.

Key Takeaways

- Patent density in Wi‑Fi 8 and early 6G is rising faster than past generations, creating a tougher SEP landscape.

- SEP positioning now drives royalty exposure, M&A value, supply chain strength, and market access.

- Cloud, AI chipmakers, automotive, and industrial tech firms are reshaping cross‑licensing and portfolio balance.

- Litigation and regulatory actions across major regions are key to licensing leverage and monetization.

- Strong patent quality, early standards involvement, and smart timing matter more than portfolio size.

Introduction

The Next-Generation Connectivity Standards Are Reshaping Patent Strategy. Wireless standardization is entering a more complex phase as Wi-Fi 8 standard development and 6G Advanced technology research accelerate across global standards bodies. As Wi‑Fi 8 (IEEE 802.11bn) moves forward in IEEE groups and 6G research expands in 3GPP, the landscape around Standard Essential Patents (SEPs) and wireless standards patents is shifting. Unlike earlier cycles that tracked incremental radio upgrades, the new wave brings AI‑native designs, ultra‑low latency, wider spectrum use, immersive computing, and industrial reliability. These advances raise both the volume and value of SEP portfolios and Wi-Fi 8 patents across the telecom ecosystem. For executives, SEP positioning now shapes royalty costs, M&A worth, supply chain strength, and market access. Patent strategy can no longer sit as a back‑office legal task. In this article, we will explore rising patent density across generations, the evolution of SEP families in wireless standards, increasing cross-licensing pressures, the role of established leaders alongside new innovators, global litigation strategies, and how portfolio strength aligns with monetization timing.

Rising Patent Density Across Generations

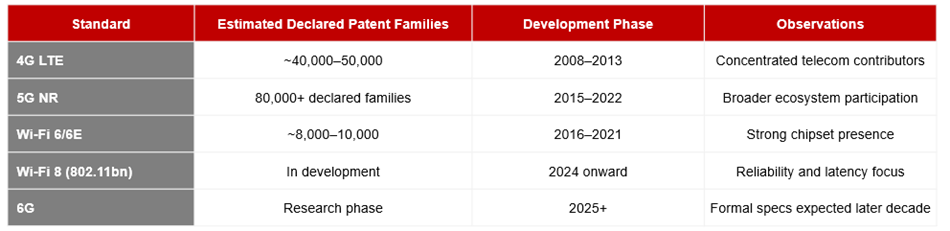

Patent declarations grew sharply from 4G to 5G, highlighting the expanding wireless patent race across connectivity standards. Analytics platforms such as IPlytics show that declared 5G patent families far outpaced LTE volumes, reflecting broader industry participation and greater system complexity. While declared patents are not the same as legally confirmed essentials, they serve as a strong signal of competitive positioning. This generational progression highlights a clear density shift. Each new standard brings more technical layers, more contributors, and a heavier concentration of SEPs. The trend underscores how patent portfolios are becoming central assets in the race for next‑generation connectivity. This trend is expected to intensify with Wi-Fi 8 technology and the emerging 6G patent landscape.

Declared SEP Families Across Wireless Generations

Wi‑Fi 8 standard development (IEEE 802.11bn) is tracked under the IEEE 802.11 working group, while 6G wireless research and 6G Advanced technology studies have entered early phases within 3GPP. Patent projections remain uncertain, but participation is broader than in earlier cycles. Cloud providers, AI semiconductor firms, and automotive companies are joining traditional telecom vendors in shaping the next generation wireless standards ecosystem, creating a more diverse contributor base. This expansion is driven by three factors. Wi‑Fi 8 focuses on deterministic latency and multi‑AP coordination, while 6G explores AI‑native management, sub‑THz spectrum, and new security frameworks. Contributor diversity has grown, with engagement spanning telecom, hyperscale cloud, semiconductor innovators, and vertical industries. Declaration strategies are also more proactive, with companies moving earlier to secure portfolio positions. The result is a denser SEP environment with greater overlap, tougher negotiations, and higher strategic complexity.

Cross-Licensing Under Increasing Pressure

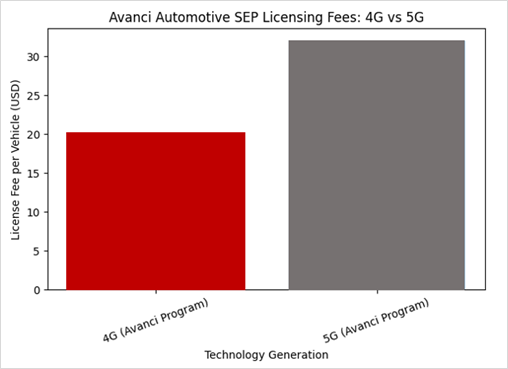

Traditional cross-licensing agreements depended on relative SEP portfolio symmetry among major telecom players. among major telecom players. As connectivity standards now intersect with automotive, enterprise networking, XR, and IoT ecosystems, that symmetry is weakening. Public licensing programs provide clearer benchmarks than speculative royalty stacking models. For example, the Avanci automotive licensing platform publicly lists a 4G license fee of approximately $20 per connected vehicle and a 5G license fee around $32 per vehicle under its program. These flat per-unit rates reflect industry efforts to move away from percentage-of-device-value debates in high-value markets such as automotive.

Enterprise Wi-Fi and IoT licensing economics are less transparent. In many cases, SEP value is embedded upstream through chipset-level licensing, reducing visible line-item royalties but maintaining monetization flows. Portfolio asymmetry is producing observable consequences. Vertical integration is increasing where SEP strength materially affects bargaining leverage. Patent pools are evolving, though fragmentation remains. Litigation activity across Germany, the United Kingdom, China, and the United States continues to shape rate expectations and enforcement leverage. As the number of wireless standards patents increases, companies must refine their SEP licensing and patent monetization strategies.

Established Leaders Versus Emerging Innovators

Next‑generation standards show clear asymmetry. Established infrastructure and chipset firms hold large portfolios, governance expertise, and litigation strength. Emerging innovators bring niche technologies such as advanced MIMO or optimization tools but lack broad portfolios. In Wi‑Fi 8, traditional chipset leaders keep strong positions, while AI‑focused entrants hold smaller clusters of claims with limited cross‑licensing power. In 6G research, cloud providers focus on virtualization and distributed intelligence. Their claims differ from radio‑layer portfolios, and it is unclear if they will scale into major SEP holdings. Geopolitics adds another layer. Chinese entities hold a large share of declared 5G patent families. At the same time, regulators are tightening oversight. The European Commission has proposed new rules to improve transparency and predictability in SEP licensing. Regulation now stands as a strategic factor alongside technical innovation.

Litigation Geography and Forum Strategy

Global SEP litigation outcomes differ widely across jurisdictions. Germany remains attractive for SEP litigation strategy and injunction-driven enforcement. The United Kingdom has shown readiness to set global FRAND rates in select disputes. The United States focuses on damages frameworks, especially after the eBay ruling that limited automatic injunctions. Meanwhile, China is becoming more influential in global licensing discussions. For companies building Wi‑Fi 8 and 6G portfolios, litigation planning must align with commercial goals. Relying on uniform enforcement assumptions is risky. Success now depends on tailoring patent strategies to jurisdictional realities and integrating them with broader business objectives.

Portfolio Strength and Monetization Timing

The strength and timing of SEP portfolios and wireless patent portfolios are becoming critical, in next‑generation connectivity. Companies can no longer rely on sheer declaration numbers or slow licensing cycles. Courts, regulators, and industry counterparts now demand higher essential patent validation and claim quality and faster engagement. Aligning portfolio development with commercialization timelines is essential to maximize value and maintain competitive advantage.

- Patent Quality Over Volume As declaration density rises, courts and counterparties scrutinize essentiality and validity more closely. Past essentiality studies show that only a fraction of declared patents survive validation. Strong portfolios now depend on robust claims, accurate technical mapping, and enforceability rather than sheer numbers. Quality is becoming the decisive factor in competitive positioning.

- Shortening Monetization Windows Technology cycles are accelerating. Wi‑Fi 6 adoption scaled quickly, followed soon by Wi‑Fi 7 commercialization. 6G research began even before 5G reached global maturity. This speed compresses monetization windows. Companies that delay licensing risk losing peak leverage before the next generational shift. Timely engagement is essential to maximize portfolio value.

Strategic Outlook

The convergence of Wi-Fi 8 technology and 6G Advanced technology research marks a turning point in telecom patent strategy. Patent density is rising. Contributor diversity is expanding. Bargaining asymmetry is growing. Regulatory oversight is increasing. Competitive strength will not depend on declaring the most patents. It will depend on combining R&D investment, standards participation, portfolio quality, licensing posture, and jurisdictional readiness into one business capability. Connectivity standards power almost every digital device. In this environment, SEP strategy is central to long‑term positioning.

Recommendation for Stakeholders

- Telecom Infrastructure & Chipset Vendors

- Strengthen early participation in standards to build strong SEP portfolios and wireless standards patents.

- Preserve cross‑licensing leverage as portfolio symmetry declines.

- Align litigation planning with long‑term commercial goals instead of reactive enforcement.

- Automotive, IoT & Enterprise Implementers

- Assess SEP royalty exposure and automotive connectivity licensing risks across multiple wireless standards.

- Begin licensing negotiations early to avoid peak‑cycle disadvantages.

- Explore pool participation or chipset‑level strategies to manage cumulative SEP risk.

- Cloud Providers & Emerging Technology Contributors

- Convert AI-driven architectures into defensible SEP portfolio strategies aligned with future connectivity standards.

- Build partnerships or pursue portfolio aggregation to enhance bargaining power in cross‑industry negotiations.

- Align patents with market applications and standards to maximize commercialization opportunities.

- Regulators & Policy Makers

- Increase transparency in SEP licensing frameworks.

- Promote balanced enforcement across jurisdictions to reduce litigation uncertainty.

- Encourage fair participation from both established leaders and emerging innovators.

- Investors & Corporate Strategy Teams

- Evaluate portfolio quality and monetization timing as part of valuation models.

- Factor in regulatory shifts, litigation risks, and cross‑industry licensing dynamics.

- Strong SEP positioning can directly influence long‑term market access and growth potential.